EVIEWS操作各种模型学习.docx

EVIEWS操作各种模型学习.docx

- 文档编号:10288777

- 上传时间:2023-05-24

- 格式:DOCX

- 页数:58

- 大小:2.26MB

EVIEWS操作各种模型学习.docx

《EVIEWS操作各种模型学习.docx》由会员分享,可在线阅读,更多相关《EVIEWS操作各种模型学习.docx(58页珍藏版)》请在冰点文库上搜索。

EVIEWS操作各种模型学习

章、图形基础与回归

原始数据

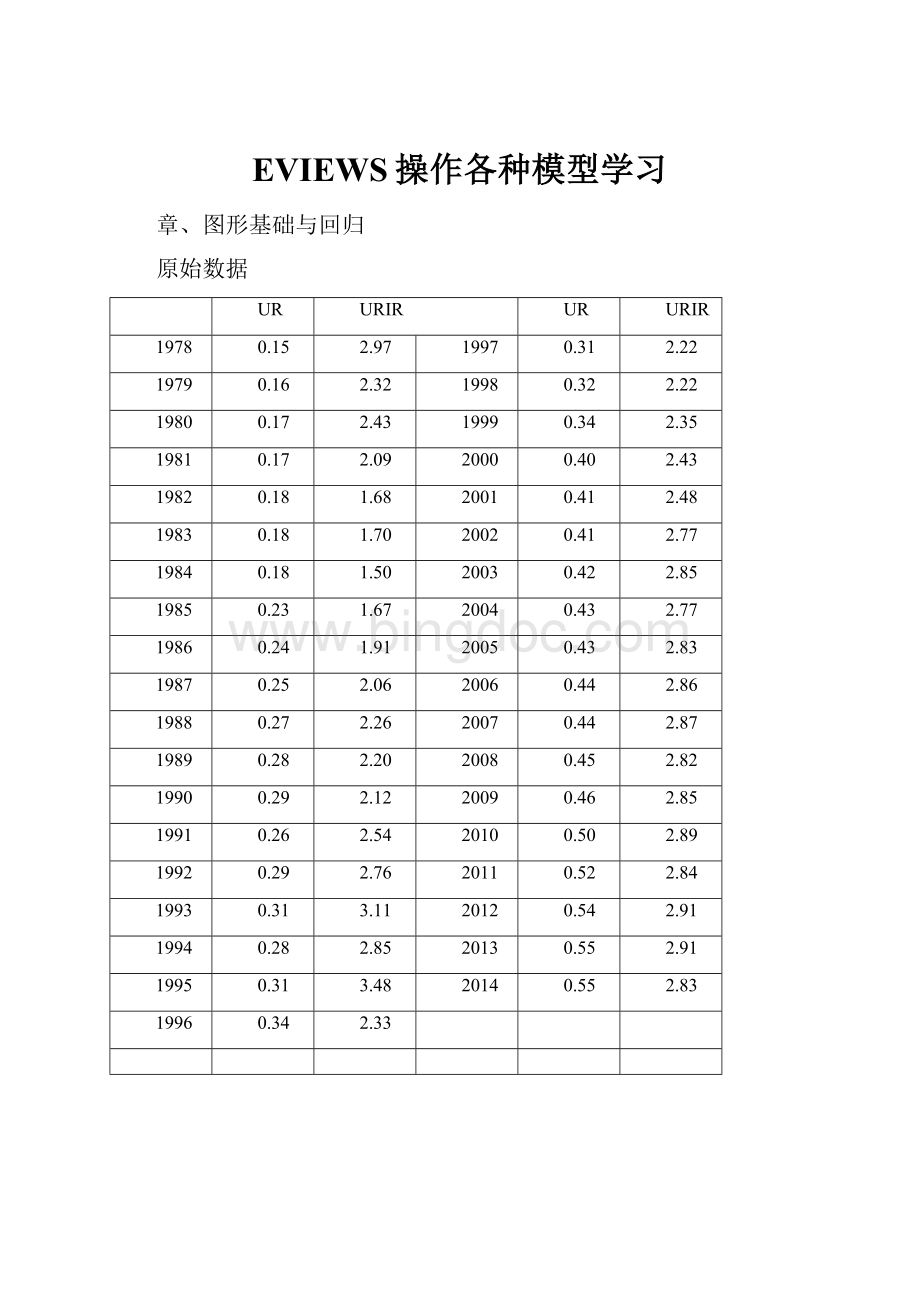

UR

URIR

UR

URIR

1978

0.15

2.97

1997

0.31

2.22

1979

0.16

2.32

1998

0.32

2.22

1980

0.17

2.43

1999

0.34

2.35

1981

0.17

2.09

2000

0.40

2.43

1982

0.18

1.68

2001

0.41

2.48

1983

0.18

1.70

2002

0.41

2.77

1984

0.18

1.50

2003

0.42

2.85

1985

0.23

1.67

2004

0.43

2.77

1986

0.24

1.91

2005

0.43

2.83

1987

0.25

2.06

2006

0.44

2.86

1988

0.27

2.26

2007

0.44

2.87

1989

0.28

2.20

2008

0.45

2.82

1990

0.29

2.12

2009

0.46

2.85

1991

0.26

2.54

2010

0.50

2.89

1992

0.29

2.76

2011

0.52

2.84

1993

0.31

3.11

2012

0.54

2.91

1994

0.28

2.85

2013

0.55

2.91

1995

0.31

3.48

2014

0.55

2.83

1996

0.34

2.33

UR

-raESZ一os①三ueno

76543210

-PULIONjoSQsueno

URIR

:

、分布图:

JB〉3判断为正太分布

S是偏度

K是峰度

5-t

Series:

UR

Sample137

4-

Observations37

3-

2-

MeanMedianMaximumMinimumStd.Dev.

SkewnessKurtosis

0.336145

0.312400

0.547000

0.15087-

0.120626

0.143256

1.887565

Jarque-Bera2.034384

Probability0.361609

0.2

0.3

0.4

0.5

三、UR的单因素联表

TabulationofUR

Date:

09/05/15Time:

21:

25

Sample:

137

Ineludedobservations:

37

Numberofcategories:

5

Value

Count

Percent

Cumulative

Count

Cumulative

Percent

[0.1,0.2)

7

18.92

7

18.92

[0.2,0.3)

9

24.32

16

43.24

[0.3,0.4)

6

16.22

22

59.46

[0.4,0.5)

11

29.73

33

89.19

[0.5,0.6)

4

10.81

37

100.00

Total

37

100.00

37

100.00

四、协方差与相矢丫生

CovarianeeAnalysis:

Ordinary

Date:

09/05/15Time:

21:

40

Sample:

137

Ineludedobservations:

37

Covarianee

Correlation

UR

URIR

UR

0.014157

1.000000

URIR

0.033170

0.204852

0.615934

1.000000

Date:

09/05/15Time:

21:

44

Sample:

137

Ineludedobservations:

37

Correlationsareasymptoticallyconsistentapproximations

URrURIR(-i)

UR,URIR(+i>

Oi

Oi□i

匚匸匚匚匸匚匚

lag

lead

0

0.6159

0.&159

1

0.5767

0.6549

2

0.4997

0.6515

3

0.4282

0.6384

4

0.3795

0.5755

5

0.3621

0.4990

6

0.3267

0.4159

7

0.3292

0.2918

8

0.2983

0.1732

9

0.2585

0.0795

10

0.1997

0.0124

11

0.1420

-0.0556

12

□0809

-0.0998

13

0.0097

-0.1538

14

-0.0231

■0.1740

15

-0.033B

-0.1790

16

-0.0565

*0.1401

17

-0.0433

-0.1238

18

-0.0316

-0.0532

19

-0.0395

-0.0939

20

-0.1629

-0.1381

1.0

0.8

0.6

0.4

0.2

0.0

1.0

0.8

0.6

0.4

0.2

0.0

五、CDF经验分布图

URIR

UR

图

QQ-亠'八

UR

QuantilesofUR

URIR

6

I

.2

■

.3

I

.4

I.5

.6

QuantilesofURIR

84

22

o

2

6

2

6

3

4

2

2

3o

2

1—

1-

七、回归散点图

UR

邻近拟合散点图:

(分布回归的结

果)

3.6

$O

八、实际值、拟合值、残差值折线图

九、回归模型预测

URF—±2S.E

Forecast:

URF

Actual:

UR

Forecastsample:

137

Ineludedobservations:

37

RootMeanSquaredError0.093736

MeanAbsoluteError0.072711

MeanAbs.PercentError25.93140

TheilInequalityCoefficientO.133790

BiasProportion0.000000

VarianeeProportion0.237674

CovarianeeProportion0.762326

十、两回归系数的联合检验置信区间是一个椭圆区域

!

八一、Wald系数约束条件检验

WaldTest:

Equation:

Untitled

RestrictionsarelinearincgeAI匚ients

TestStatistic

Value

df

Probability

F-statisticChi-square

272.1503

(1.35)

0.0000

272.1503

1

0.0000

NullHypothesisSummary:

NormalizedRestriction[=Q)

Value

Std.Err,

-1+C

(1)+C

(2)

-0,907527

0.055012

Chow分割点检验结果

ChowBreakpointTest1991

NullHypothesis:

Nobreaksatspecifiedbreakpoints

Varyingregressors:

AllequationvariablesEquationSample:

19782014

F'Statistic

11.00551

Prob.F(2r33)

0.0002

Loglikelihoodratio

18.90797

ProbJChi-Square

(2)

0.0001

WaldStatistic

22.01103

Prob.Chi-Squa(e

(2)

0.0000

F、LR的P值显著,表示:

模型无显著的结构变化

十二、Chow稳定性检验(p75)

Chow预测结果:

ChowForecastTest:

Forecastfrom1991to2014

F-statistic

Loglikelihoodratio

4.744782

89.83840

PfOb.F(24,11)

Prob.Chi-Square(24)

0.0050

0.0000

TestEquation:

DependentVariable:

URMethod:

LeastSquares

Date:

09/07/15Time:

10:

31

Sample:

197S1990

Ineluded!

observations:

13

Coefficient

Std.Errort-Statistic

Prob.

URIR

C

-0014716

0.241289

0.037436・0393094

0.0787753.063016

07018

0.0100

R-squared

AdjustedR-squared

S.Eofregression

SumsquaredresidLoglikelihoodF-statistic

Prob(F-statistic)

0.013853

*0.075797

0.051024

0.028637

21.32073

0.154523

0.701762

Lieandependentvar

S.Ddependentvar.Akaikeinfocriterion

SchwarzcriterionHannan-Ouinncriter.

Durbin-Watsonstat

0.210827

0.0491932972421・2.885505・

2990286

0.127458

十三、零均值附近的递归残差曲线图

★注:

红线为5%的临界值线,在1991年后的CUSUM曲线变得十分陡哨,说明:

回归方程系数并不是稳定的。

One-Step

Probability

Recursiv

eResiduals

3.—步预测检验:

4.N步预测检验:

进行一系列的Chow检验

N-StepProbability

RecursiveResiduals

★注:

上部分是递归残差,下部分是检验显著性的概率

.3

.2

十四、White异方差检验

Obs*R-squared=10.4,其P值=0.0055表示残差存在异方差性。

F统计量表示:

检验辅助方程的整体显著性,下图中整体显著。

HeteroskedasticityTest:

White

TestEquation:

DependentVariaDle:

RESIDA2Method:

LeastSquaresDate:

09/07/15Time:

11:

02

Sample:

19782014

Irt匚ludedobservations:

37

CoefficientStd.Errort-StatisticProb.

c

URIR

URIRA2

0.039819

-0.042859

0.011780

0.0458S60.867779

0038582-1110863

0.0079411.483508

0.3916

0.2744

0.1472

R-squared

0.281447

Meandependentvar

0.008786

AdjustedR-squared

0239179

S.D.dependentvar

0013287

S.Eofregression

0.011590

Akaikeinfocriterion

-5999002

Sumsquaredresid

0.004567

£匚hwamcriterion

-5.869187

Loglikelihood

1139963

Hannar/Quinnenter.

-5953754

F-statistic

6.658663

Durbin-Watsonstat

0.374222

Prob(F-statistic)

0.003629

十五、WLS加权最小二乘法

DependentVariable:

UR

Method:

LeastSquaresDate:

09/07715Time:

11:

29

Sample:

19782014includedobservations:

37

Weightingseries:

W

Coefficient

Std.Error

t-StatisticProb.

URIR

0.168557

0.031139

5,4130330.0000

C

-0.086069

0.076542

-1.1244650.2685

WeightedStatistics

R-squared

0.455684

(Jeandependentvar

0.328603

AdjustedR-squared

0440132

S.Ddependentvar

0.100794

SE,ofregression

0.090040

Akaikeinlacriterion

*1.924588

Sumsquaredresid

0.283752

Schwarzcriterion

-1,837512

LogliKelitiaod

37.50488

HannarpQuinncriter

-1893890

F-statistic

29.30092

Durbin-Watsonstat

0.279531

Prob(F-statistic)0.000005

UnweightedStatisti匚s

R-squared

□378738

Meandependentvar

0.33614S

AdjustedR-squared

0.350987

SD.dependentvar

0.120526

S.E.ofregression

0.096427

Sumsquaredresid

0.325433

Durbin-Watsonstat

0.310271

R-SQuarecl

AdjustedR-squarecdlS.E.ofreoresslion

SLimscjuoreclresidlLoo1

11h(D F-statistic Prob(F-statistic> O„61S958OS810450.061509 0.12V852 S2.79260 MeandependentvarS.DdependentvarAKalKeinTocriterionSchwar-z・criterion MAninAn-Ouinn: crirtierDurbin-Watson O0-950292.637-453・2„4I333OO-2.S76OS6 64271O.DDOOO1 1,,204229 十六、残差自相尖图及其Q检验统计量 CorrelogramofResiduals Date: 09/07/15Time: 15: 50 Sample: 19782014 Ineludedobservations: 37 1-16阶的p值都小于0.01,说明拒绝原假设,残差序歹U存在自相尖性。 十七、残差自相矢LM检验结果 Breuscn-GocrrreyserialCorrslatJonLMT©st: F与Obs两个的P值显示: 存在自相矢 十八、Newey-West—致协方差估计 Dependentvariable: UR Method: LeastSquares Date: 09/07/15Time: 1635 Sample: 19782014 Includedobservations: 37 NeweyAVestHACStandardErrors&Covarianee(lagtruncation=3) Coefficient StdLErrort-Statistic Prob. URIR 0.161922 0.0508133,186620 0.0030 C -0.069449 0.109907-0.631837 0.5316 R-squared 0.379375 Meandependentvar 0.336145 AdjustedR-squared 0.361643 S.Ddependentvar 0.120626 S.E.ofregression 0.096377 Akaikeinfocriterion -1.788557 Sumsquaredresid 0.325099 Schwarzcriterion -1,701481 Loglikelihood 35.08831 Hannan・Quinncriter. *1.757959 F-statistic 2139474 Durbin-Watsonstat 0.289676 Prob(F-statiStic) 0.000049 十九、两阶段TSLS估计检验结果 DependentVariable: URPethod: Two-StageLeastSquaresDate: 09/07/15Time: 16: 43 Sample: 19782014 Indudedobservations: 37 InstrumentlistCUR Coefficient Std.Errort-Statistic Prob. URIR 0.426813 0.0922754.625445 0.0000 C *0732965 0.232564-3.151675 0.0033 R-squared -0.635916 Meandependentvar 0.336145 AdjustedR-squared -0.682657 S.D.dependentvar 0.120626 S.E,ofregression 0.156473 Sumsquaredredid 0856934 F-statistic 2139474 Durbin-Watsonstat 0.632913 Prob(F-statistic) 0.000049 SecontTStageSSR 4.14E*30 二十、广义矩估计GMM检验结果 toependentVariable: UR Method: GeneralizedMethodofMoments Date: 09/07/15Time: 16: 51 Sample: 19782014 Ineludedobservations: 37 Kernel: Bartlett,Bandwidth: Fixed(3).NoprewhiteningSimultaneousweightingmatrix&coefficientiterationConvergeneeachievedafter: 1weightmatrix,2totalcoefiterationsInstrumentlistCURIR Coefficient Std.Error1-Statistic Prob. URIR 0.161922 0.0509333.179114 0.0031 C -0.069449 0.112195-0.619000 0.5399 R-squared 0379375 Meandependent回 0.336145 AdjustedR-squared 0.361643 S.D.dependentvar 0.120626 S・E.ofregression 0.096377 Sumsquaredresid 0.325099 Durbin-Watsonstat 0.289676 J-statistic 1.58E-27 章、离散及受限制因变量模型 、原始数据 obs GPA SE PSI Grade 1 2.66 20 0 0 2 2.89 22 0 0 3 3.28 24 0 0 4 2.29 12 0 0 5 4 21 0 1 6 2.86 17 0 0 7 2.76 17 0 0 8 2.87 21 0 0 9 3.03 25 0 0 10 3.92 29 0 1 11 2.63 20 0 0 12 3.32 23 0 0 13 3.57 23 0 0 14 3.26 25 0 1 15 3.53 26 0 0 16 2.74 19 0 0 17 2.75 25 0 0 18 2.83 19 0 0 19 3.12 23 1 0 20 3.16 25 1 1 21 2.06 22 1 0 22 3.62 28 1 1 23 2.89 14 1 0 24 3.51 26 1 0 25 3.54 24 1 1 26 2.83 27 1 1 27 3.39 17 1 1 28 2.67 24 1 0 29 3.65 21 1 1 30 4 23 1 1 31 3.1 21 1 0 32 2.39 19 1 1 1、Logit模

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- EVIEWS 操作 各种 模型 学习

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《工程造价案例》期末考试复习题及参考答案.docx

《工程造价案例》期末考试复习题及参考答案.docx

-

《宽带IP网络》试题及答案北邮考试专用解析.docx

-

《描绘小灯泡的伏安特性曲线》试题精选.docx

-

1承诺办理时限是什么概念实际办理的时间能不能比承诺办理时限.docx

-

3年高考真题状语从句汇总含考查重点及答案.docx

-

4篇安装项目经理年终总结范文模板.docx

-

《C语言程序设计》学习指导.docx

-

《傲慢与偏见》人物性格分析.docx

-

《计算机应用实务》理论复习题.docx

-

《教育理论综合知识》试题及答案解析2.docx

-

《老人与海》上课学习上课学习教案.docx

-

《传感器技术》题库.docx

-

《C语言程序设计》习题及解答14章.docx

-

#2机组大修建议汇总.docx

-

《算法设计与分析》考试题目及答案教学内容.docx

-

《地心历险记》观后感600字600字读后感.docx

-

#对完善我国监护法律制度立法的思考.docx

-

《安全用电珍爱生命》宿舍安全用电宣传活动策划书.docx

-

《幼儿园数学教育活动指导》实践性教学方案1doc.docx

-

《1万吨年高效环保型复合活性生物菌剂15万吨年生物菌肥15万吨年生物菌饲料农业产业化技术改造项.docx

-

《工程质量检验标准》.docx

-

《财务预算学》复习思考题.docx

-

《中国诗词大会》第四季里的各类知识点汇总.docx

-

《财务会计》相关复习题英文版.docx

-

《拉丁美洲》音乐教案.docx

-

《春》学案1 1.docx

-

01人力资源战略规划与年度计划制订编写模板.docx

-

《Unit 4 Wheres my schoolbag》单元教案.docx

-

《航海雷达与ARPA》试题集72659.docx

-

《哪吒之魔童降世》电影观后感5篇观《哪吒之魔童降世》有感.docx

-

《第5单元 化学方程式》九年级化学单元练习.docx

-

1吨每小时纯净水设计方案.docx

-

统编版语文一年级上期末复习知识要点.docx

-

低碳环保作文800字20篇.docx

-

高二地理清明假期练习.docx

-

高二作文之高中运动会演讲稿.docx

-

学年八年级语文下册单元检测试题.docx

-

地下室防水施工方案#3.docx

-

高考地理第五章 自然地理环境的整体性和差异性 第一节 自然地理环境的整体性.docx

-

高考地理选择题专项突破一.docx

-

高考物理专项冲击波讲练测系列 专题27 分子动理论和热力学定律.docx

-

弟子规全文拼音解释版.docx

-

高考英语二轮复习 完形填空月练5.docx

-

高三历史上学期第一次统练试题.docx

-

第08章 氢的输送及加注.docx

-

高三文科《三国演义》竞赛.docx

-

高三语文古诗常见意象例析.docx

-

第五章 风化作用与剥蚀作用.docx

-

服务质量管理DOC.docx

-

高中生物必修二精选精彩试题及解析汇报.docx

-

电大《国际礼仪概论》教案.docx